Quarterly Considerations – Q3 2025

Policy Clarity and Market Momentum

Q3 began with Treasury issuing new start-of-construction guidance for projects seeking qualification under the OBBB’s technology-neutral Section 45Y and Section 48E tax credits.1IRS Notice 2025-42 The update clarified the physical work test and four-year continuity requirement for developers, removing the previous 5% safe-harbor option for wind and solar projects above 1.5MW. This shift has already influenced how developers and lenders structure qualification strategies, as many moved quickly to secure eligibility before the September 2, 2025 deadline.

Start-of-Construction (“SoC”) Qualification Methods

| Tax Credit | Technology | SoC Timing | SoC Qualification |

|---|---|---|---|

| 48E & 45Y | Wind & Solar > 1.5 MW | Before Sept 2, 2025 | 5% safe harbor or physical work test + continuity requirement |

| 48E & 45Y | Wind & Solar > 1.5 MW | Between Sept 2, 2025 and July 4, 2026 | Physical work test + continuity requirement |

| 48E & 45Y | All Other Technologies, except for Wind & Solar >1.5MW | Before Dec 31, 2033 (for full credit amount) | 5% safe harbor or physical work test + continuity |

| 48 & 45 | Wind & Solar | Before January 1, 2025 | 5% safe harbor or physical work test + continuity |

Project Finance Trends

Start-of-Construction Strategies Intensify

Developers are actively pursuing start-of-construction strategies to qualify mid- to late-stage projects. Many are securing contracts for the off-site manufacturing of custom-built components, while others are initiating on-site physical construction. The limited availability of custom-built components for distributed generation (DG) projects is prompting developers to collaborate with manufacturers to develop tailored qualification strategies.

In response to developer demand for tax credit qualification, lenders are broadening their equipment financing offerings. These solutions are enabling developers to secure critical components and lock in eligibility under safe harbor provisions.

Tax Credit Buyers Settle in Post-OBBB

The OBBB has reshaped future tax liability expectations for many companies. Corporate tax teams are progressing toward more precise capacity forecasts and are expected to re-enter the market with targeted mandates.

Buyers are also expanding into new credit types beyond traditional solar and wind, particularly Section 45Z production tax credits, which received a two-year extension and improved carbon-intensity treatment under OBBB. These enhancements have made 45Z credits appear less politically vulnerable, increasing their appeal.

Flight to Quality Shapes Capital Deployment

Tax capital investors and lenders continue to prioritize sponsor quality, execution certainty, and historical performance. Sponsors with proven track records, robust capital backing, equipment inventory, and flexible balance sheets are best positioned to secure favorable pricing. Investor selectivity remains high, reflecting the emphasis on execution certainty and sponsor quality in the post-OBBB environment. Beyond financing dynamics, transaction activity across the renewables sector remained steady in Q3 as developers and investors adapted to evolving policy and demand trends.

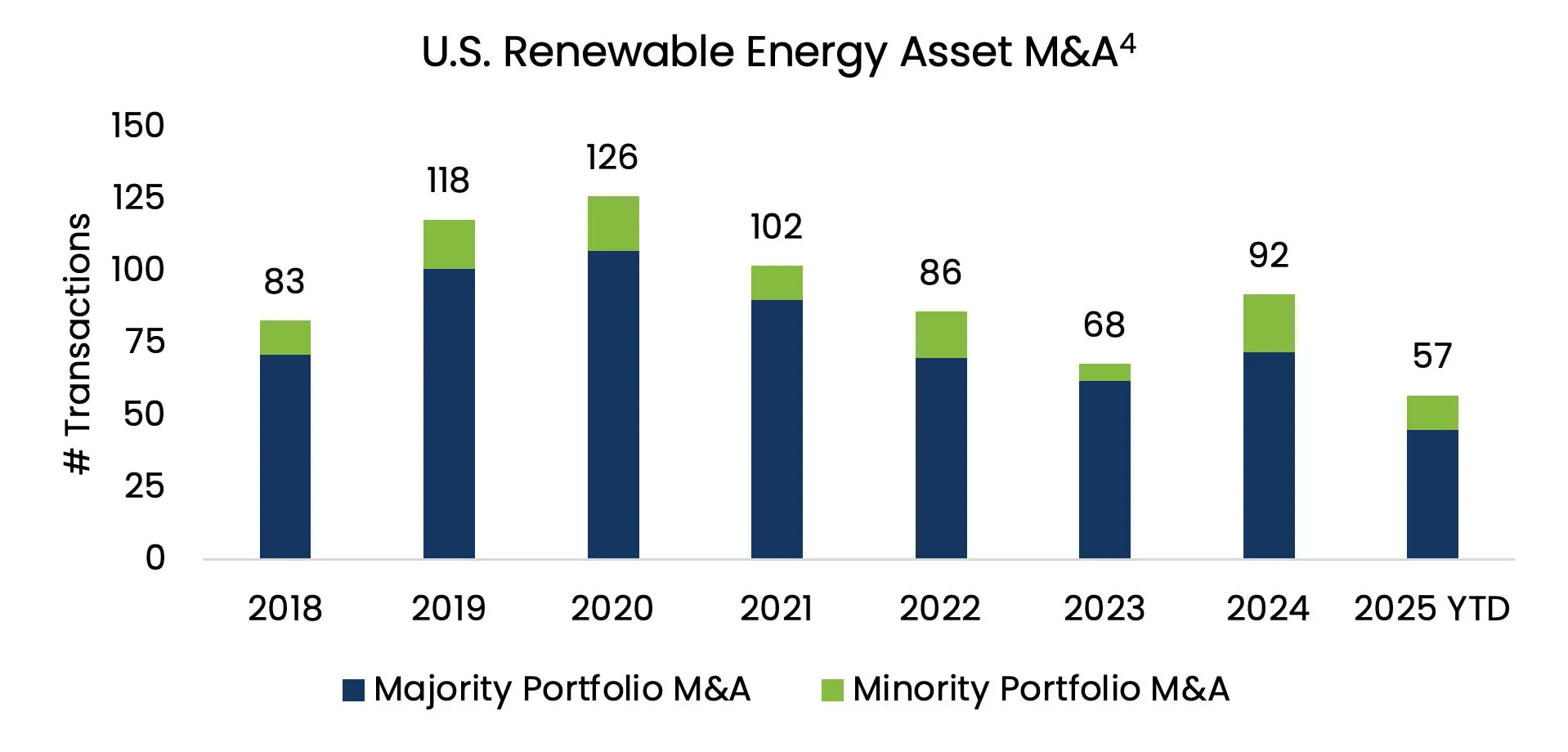

M&A Trends

Resilient Market Activity

Q3 M&A volume in the U.S. solar sector remained steady despite macro uncertainty, supported by strong structural tailwinds in demand and an evolving mix of strategic and financial buyers. Developers accelerated spend ahead of the September 2nd safe-harbor deadline, temporarily tightening module supply and pushing pricing up 3–4% to roughly $0.28/W as demand was pulled forward.2PV Magazine: Policy Deadline Rush Pushes U.S. Solar Module Pricing Up in Q3, October 8, 2025 We expect this short-term price pressure to normalize as safe-harbor-driven demand eases and procurement pipelines reset.

Hyperscalers Drive Offtake Growth

The center of gravity for offtake growth has shifted to hyperscalers. Data center expansion is driving significant levels of corporate PPAs. Major technology firms like Microsoft, Meta, and Amazon are now serving as anchor offtakers for new utility-scale and hybrid solar-plus-storage projects, including Microsoft’s 475 MW solar offtake with AES, Meta’s 791 MW agreement with Invenergy, and Amazon’s partnership with Avangrid in Oregon.3Data Center Dynamics: Microsoft Signs Solar PPAs totaling 475MW with AES, March, 20, 2025 This trend reinforces long-term demand visibility and supports premium valuations for developers with strong execution track records.

Consolidation and Capital Recycling Continue

CRC-IB continues to see consolidation across both distributed generation and utility-scale platforms. Recent transactions include Clearway’s acquisition of 833 MWdc of operating solar assets from Deriva Energy, Ares Management’s purchase of a 49% stake in EDPR’s U.S. portfolio, and TPG’s take-private of Altus Power. These examples signal sustained interest in scale, operating stability, and balance-sheet-light development models. Strategic players are re-evaluating their footprints, i.e., BP’s potential sale of a 50% stake in Lightsource bp, reflecting a broader trend of oil majors seeking to recycle capital and co-fund expansion5Reuters: BP Seeks to Sell 50% of Solar Unit to Strategic Partner, Bids Due in June, Document Shows, March 13, 2025.

Defining Attributes of Attractive Platforms

- Hybridization as the default configuration Utility-scale pipelines are now routinely paired with 2- to 4-hour storage to meet RFP requirements and provide evening shaping demanded by hyperscalers and utilities.

- Asset rotation and balance-sheet discipline: Developers are monetizing operating portfolios or minority stakes to recycle equity into new projects while maintaining development upside.

The sector continues to navigate a “policy torque” environment, characterized by shifting tariff regimes, evolving domestic content and origin rules, and shortened credit-eligibility windows. These dynamics introduce execution risk but also create differentiated opportunities for well-capitalized and agile platforms. Capital has become more selective, favoring proven operators capable of disciplined capital recycling, structured partnerships, and JV-led growth rather than pure balance-sheet builds.

Looking ahead, near-term growth may remain uneven due to the safe-harbor rush and regulatory uncertainty, but long-term fundamentals remain intact. Load growth from electrification and digitalization, the accelerating pairing of solar and storage, and continued hyperscaler offtake underpin a strong medium-term M&A outlook.

CRC-IB’s Recently Completed Transactions

| Counterparty | Sponsor | CRC-IB Role | Date | Transaction Synopsis |

| Confidential | Confidential | Exclusive Financial Advisor | 9/2025 | Preferred Equity Financing for Battery Storage Project |

| Confidential | Confidential | Financial Advisor to Sponsor | 9/2025 | Tax Equity Financing for Utility-Scale Solar Project |

| MUFG, First Citizens Bank, ING, National Bank of Canada, Cadence, Siemens, Advantage Capital | Dimension Energy | Exclusive Financial Advisor | 9/2025 | Tax Equity & Debt Financing for 134 MWDC Community Solar Portfolio |

| First Citizens Bank, East West Bank | Alpha Omega Power | Exclusive Financial Advisor | 8/2025 | Tax Equity Financing for 200 MW / 400 MWh Battery Storage Project |

| Confidential | Greenflash Infrastructure | Financial Advisor to Sponsor | 8/2025 | Preferred Equity, Transfer & Debt Financing for 400 MW / 800 MWh Battery Storage Project |

| Foss & Company | Innergex Renewable Energy | Exclusive Financial Advisor | 7/2025 | ITC Transfer for 30 MWAC Solar + 30 MW Storage Project |

| Confidential | Gore Street Energy Storage Fund | Financial Advisor to Sponsor | 7/2025 | ITC transfer for 200 MW / 400 MWh Battery Storage Project |

References

- IRS Notice 2025-42

- PV Magazine: Policy Deadline Rush Pushes U.S. Solar Module Pricing Up in Q3, October 8, 2025

- Data Center Dynamics: Microsoft Signs Solar PPAs totaling 475MW with AES, March, 20, 2025

- Announcements tracked from inframationnews.com and available press releases through September 2025

- Reuters: BP Seeks to Sell 50% of Solar Unit to Strategic Partner, Bids Due in June, Document Shows, March 13, 2025